You’ve no doubt heard of them on financial news networks and even mainstream media. When companies go public, it’s typically through an initial public offering (IPO). Let’s delve into IPOs.

What is an IPO?

The initial public offering (IPO) is a process that transforms a privately owned company into a publicly traded company.

The term “going public” is synonymous with being “publicly listed” and “publicly traded” all pertain to the IPO process.

Prior to the IPO, companies will usually go on a “road show” to various institutions and accredited investors to drum up demand for its shares. The night before the actual IPO, the underwriters will agree on a price and total number of shares offered (IE: 22 million shares offered at $30). This is the proceeds of the IPO, however, it’s not necessarily the price at which shares will be available to the public in the “aftermarket”.

The aftermarket applies to trades made after the company goes public. Depending on the demand, shares may actually “open” much higher (IE: IPO shares open at $50 which priced at $30). After the first trade is completed, the company is officially public, and shares are actively traded in the aftermarket.

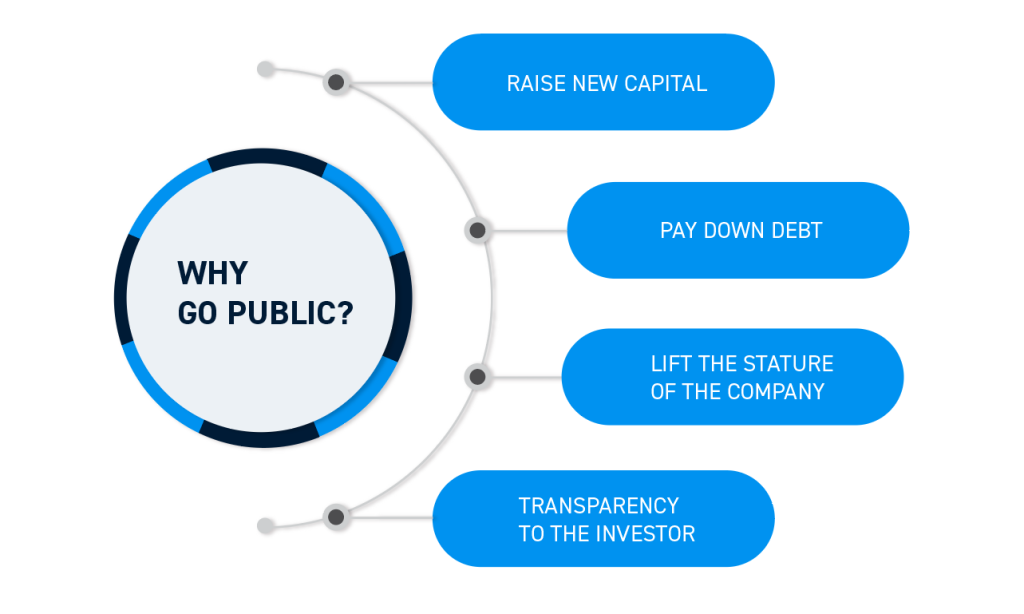

Why Would a Company Go Public?

Private companies that wish to raise capital while providing liquidity for early investors may consider going public. Being a public company provides more transparency for new investors and also lifts the stature and reputation of the underlying company depending on which exchange its listed on. Companies may wish to go public primarily to raise new capital to pay down debt, gain more working capital, or invest back into the company.

Common Types of IPOs

Traditional

The traditional IPO utilizes underwriters which are investment banks to pitch their stock to the clients as well as analysts to provide coverage. New shares are usually issued and sold to the public which will then take an ownership stake but not necessarily a voting stake in the company.

Usually, one share of common stock enables one vote, however, a separate class of shares can be created to enable majority voting power to the management and or founders. Traditional IPOs come with lock-up provisions which limit the number of shares that can be sold by insiders and beneficial owners. This prevents the potential for dilution.

Direct Listing

A direct listing doesn’t use underwriters and sells existing shares to the public. In other words, the insiders and beneficial owners sell their own shares to the public and the company usually receives no proceeds.

This is mostly a liquidity event that enables early investors to cash out part of all of their shares into the liquidity created by the direct listing. There is no traditional “lock-up period” which means insiders can sell shares (in accordance company bylaws) anytime. There is little chance of dilution since there are no new shares being created for the IPO.

Since investment banks are not involved in a direct listing, excess volatility can be extreme at times since there are no clear leader market makers. The price action is purely based on market supply and demand without interference from underwriters who may decide to support a particular price level.

How Does a Company Choose an IPO Price?

The IPO price is usually determined by the underwriters as they assess the demand for the issue in conjunction with the company executives. Keep in mind that an S-1 Registration Statement needs to be filed before the pricing.

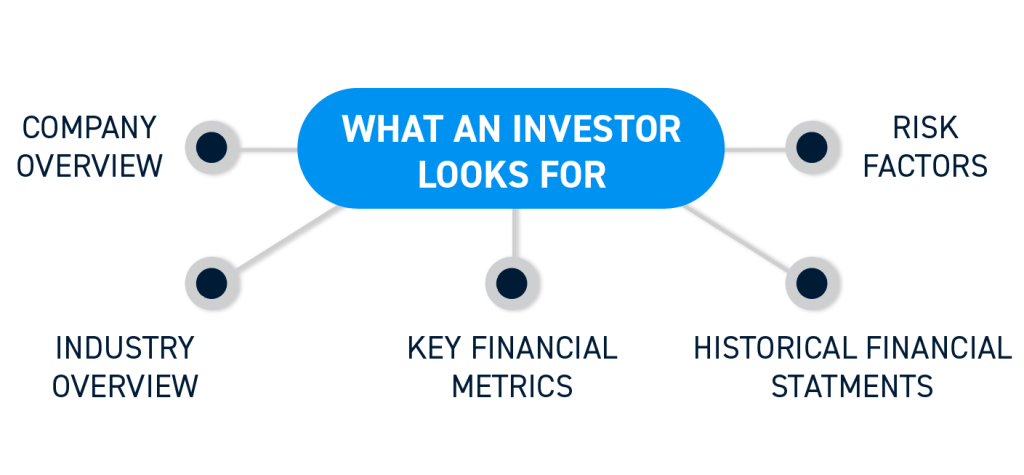

The S-1 gives investors a first look at the inner workings of the company including historical financial statements, key financial metrics, company overview, risk factors, industry overview, strategic goals and much more.

The final pricing for shares is determined on the night before the IPO as bankers meet with management pricing the deal based on orders and demands. Once the offering price is finalized, the investment banks will allocate shares. Keep in mind the IPO process is time consuming taking anywhere from six months to a year and costly.

Things Traders Should be Aware of When Trading IPOs

Investors may view IPOs as opportunities to invest in new companies. Traders generally take a different approach. Here are some things traders should be aware of when considering trading an IPO.

It’s Hard to gain an Edge –

From a trader’s perspective, there is little to no edge as the IPO starts trading. Charts and indicators offer no real edge unless you are a pure day trader since there is not enough data to generate daily or weekly charts. With trading usually hot and heavy on the first day caution should be exercised.

Don’t Stray from Your Core Strategy

It’s easy to fall for the hype when it comes to more popular IPOs. It’s not uncommon to have long anticipated IPOs hit mainstream media to pull in mom-and-pop investors who are familiar with the company and/or its products. Be aware that the smart money may have already entered long before the IPO, or have been allocated IPO shares to unwind in the aftermarket. Stick to you core methodology if trading IPOs.

Lock-Up Periods

While IPOs allocate a finite number of shares in the offering, three are much more shares looming when the lock-up period ends.

Lock-up periods determine when the insiders can sell their shares. The information on lock-up expiration is usually found in the S-1 Registration Statement explaining the terms of the lock-up. For example, XYP may be offering 5 million shares priced at $20 on their IPO, the lock-up period is six-months after the IPO when 50 million shares are free to be sold.

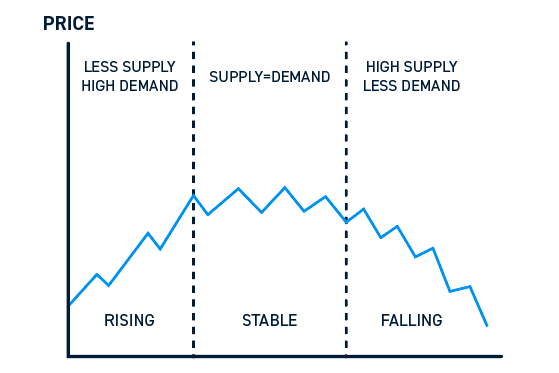

Knowing the length of lock-up periods and the exact date of expiration is a dilution strategy that could provide a slight edge to traders. In theory, a stock should sell off when more shares are floated to the public and bounce when that ends. As with any trading strategy, however, other factors may come into play and traders need to adjust accordingly.

Short Selling

As determined by the Securities and Exchange Commission (SEC), which is in charge of IPO regulation in the United States, the underwriters of the IPO are not allowed to lend out shares for a short sale for 30 days. On the other hand, institutional and retail investors can lend out their shares to investors who want to short them.

Options Trading

Usually, IPO stocks with a heavy following may get options trading after 30 days from the IPO. Options enable the ability to short-sell via put contracts. Stocks may rise on the announcement of options trading availability for IPOs. This doesn’t apply to all IPO stocks, usually just the highest volume popular issues.

How Can Traders Keep Track of IPO’s?

If you are still interested in trading IPOs, then you can be proactive in finding them and researching them. There are many sites online that will provide details of upcoming IPOs. Additionally, the most hyped up and anticipated IPOs will be publicized on the financial news networks.

As previously mentioned, traders should be careful about buying into the hype. Once you find the IPO that suits your tastes, make sure to research it thoroughly starting with the S-1 Registration Statement, publicly traded competitors, and peers. Most IPOs are a losing game for long players on the initial day unless shares are priced at a discount. However, IPOs can be a winning play day to weeks after the IPO when (and if) they bottom out and start to climb again. Do your research and bide your time.